SOUTH FLORIDA

Home Sales Down, Average Price Up

Home sales are down 0.5% year over year, with January 2024 at 4,420 compared to 4,442 last January. Sales are up for single families and down for condos & townhomes.

- Single families: 2,064 (2023) | 2,162 (2024)

- Condos & Townhomes: 2,378 (2023) | 2,258 (2024)

Average sale price increased 11.2% year-over-year, now at $790,098 compared to $710,740 in January 2023. Prices increased across all categories.

- Single families: $948,706 (2023) | $1,058,316 (2024)

- Condos & Townhomes: $504,195 (2023) | $533,283 (2024)

Homes Listed For Sale:

The number of homes listed is up by 24% when compared to January 2023.

- 2024: 12,307

- 2023: 9,929

- 2022: 10,583

Pending Home Sales:

The number of homes placed under contract is down by 9.1% when compared to January 2023.

- 2024: 6,618

- 2023: 7,282

- 2022: 10,695

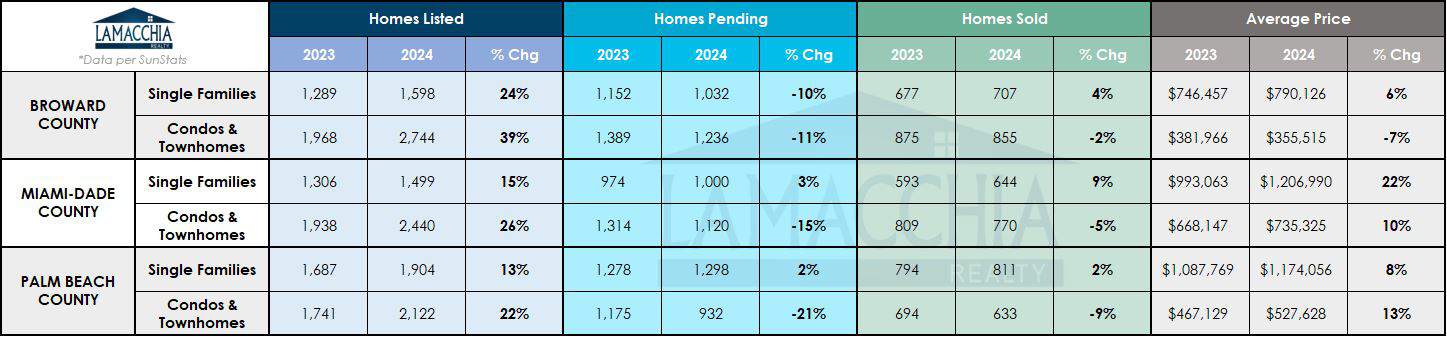

January 2024 Data by County

Data provided by SunStats then compared to the prior year.

What’s happening in the market?

We have seen significant changes to the real estate housing market over the past few years with factors constantly shifting and situations ever evolving. So far, 2024 has proven to be no different. In South Florida specifically, we are already seeing a shift towards a buyer’s market underway. As Anthony states in his 2024 predictions, even though we expect the market to continue to shift, we are not out of the woods quite yet in terms of housing market ebbs and flows.

What does this mean for Buyers?

- Despite the continuous demand to live in South Florida, inventory in South Florida over the last several months has been rising, and this month the trend continued with levels just slightly above 2021. More inventory translates to more options for buyers as well as potentially less competition and a stabilization or eventual reduction in home prices!

- Even though South Florida is a popular market for cash sales – allowing the region to be slightly less susceptible to changing mortgage rates – the majority of buyers still use traditional financing.

- As such, buyer affordability is still diminished due to increased mortgage rates and rising home prices. Therefore, now more than ever, it is important to know what mortgage options are available to you such as buydowns and assumptions. Also, make sure you are ready to strike with updated preapprovals and a plan that works best for you so you can accomplish your buying goals!

What does this mean for Sellers?

- It is important to note that the increase in inventory in South Florida can largely be attributed to condos as stricter regulations have made it more expensive to both build and maintain associations. For current condo owners, this means increased expenses such as higher monthly HOA fees, special assessments, etc. As a result, many of them are deciding to list their homes rather than assume those new challenges. In turn, condos are being listed faster than they are going under agreement which drives inventory up.

- Many sellers are still hesitating to list their homes. Remember, many sellers are also buyers so they do not want to enter the market and give up their low mortgage rate from the pandemic era. Even though inventory is rising, many are also concerned that they will not be able to find a home to move into after theirs sells.

- However, we are starting to see many want-to-be sellers starting to list their homes due to lifestyle changes such as relocating for work or divorce. If you are ready to sell your home, make sure it is priced competitively, especially condos, to generate the most demand! This gives you more leverage to negotiate which is particularly important for those looking to sell and buy at the same time!

What’s next?

If inventory in South Florida continues to rise, this should help to keep excessive price growth at bay and give buyers long-awaited options in the market – all signs of a shifting market. Important to note that mortgage rates and rising home prices continue to play a large role in consumer decision making, along with other economic factors such as inflation. Specifically, in January 2024, mortgage rates loomed close to 7%. Now, recent economic indicators have pushed those rates up past 7%. These rates majorly impact the decisions of both buyers and sellers as stated above.