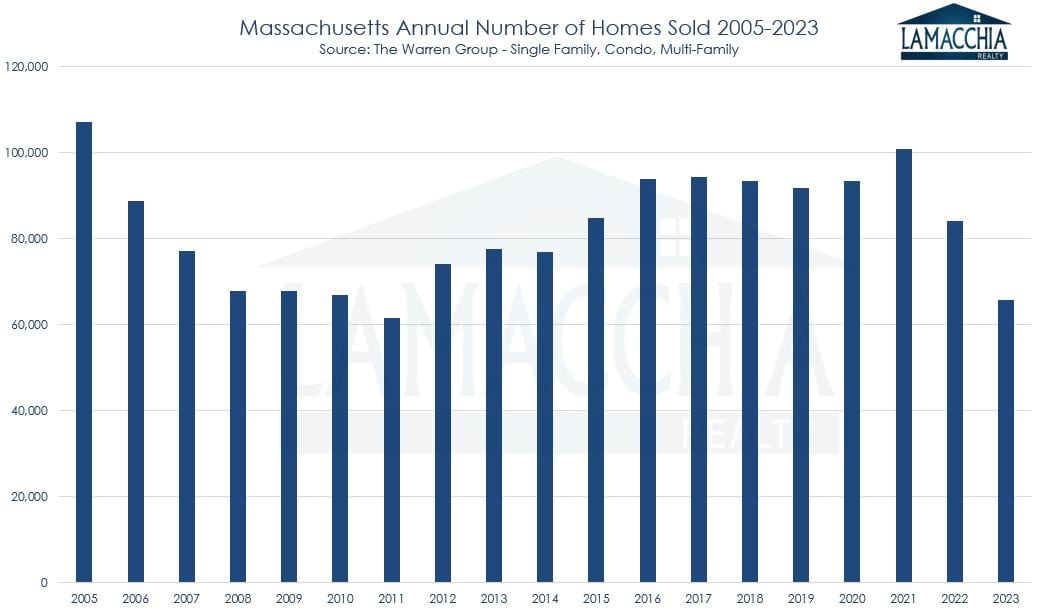

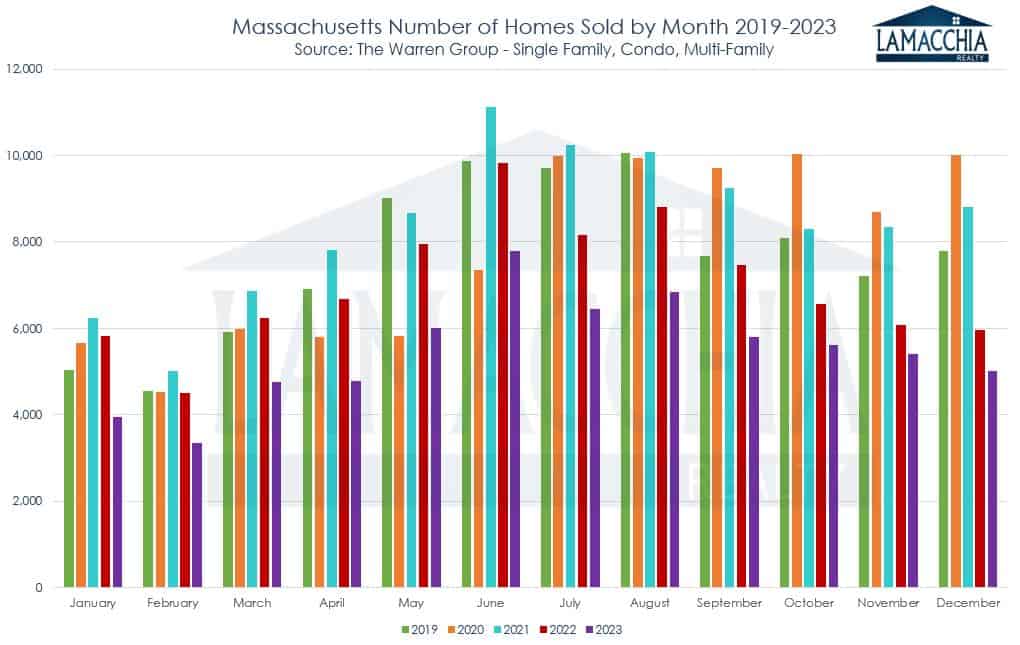

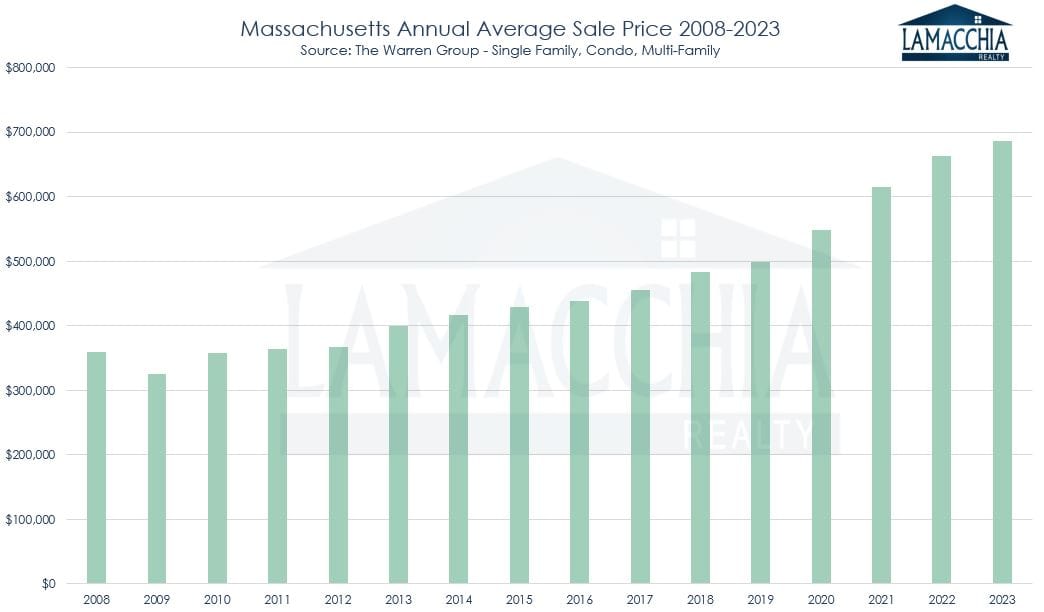

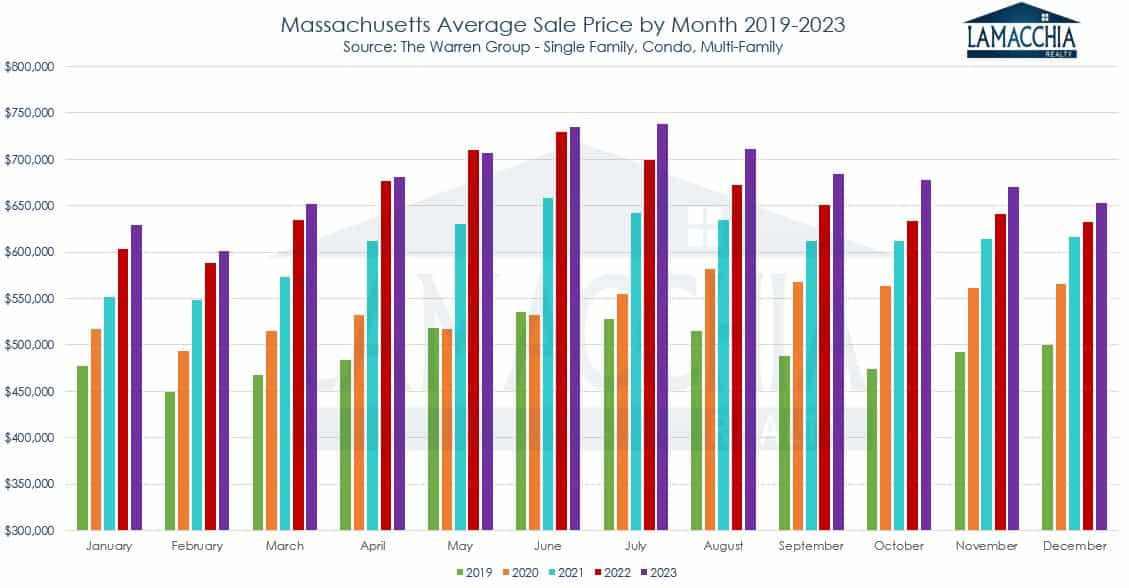

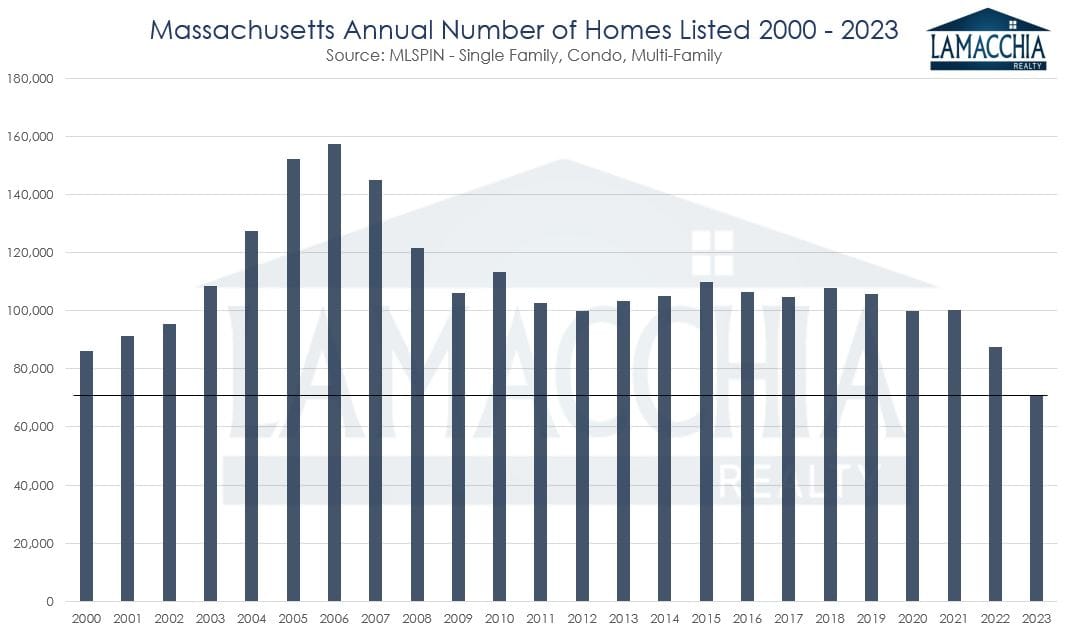

2023 was a notable year in real estate history, but if we had to put our finger on what stood out, it was how the number of homes listed was the lowest in over two decades. It kept inventory down, which propped up prices, but sales are down nearly 22%, and buyers are hungry. With rates trying to reach equilibrium after their nosedive in 2020, everyone has had to accept that pandemic-era rates are a thing of the past and therefore higher monthly mortgage payments are here to stay.

2023 was a notable year in real estate history, but if we had to put our finger on what stood out, it was how the number of homes listed was the lowest in over two decades. It kept inventory down, which propped up prices, but sales are down nearly 22%, and buyers are hungry. With rates trying to reach equilibrium after their nosedive in 2020, everyone has had to accept that pandemic-era rates are a thing of the past and therefore higher monthly mortgage payments are here to stay.

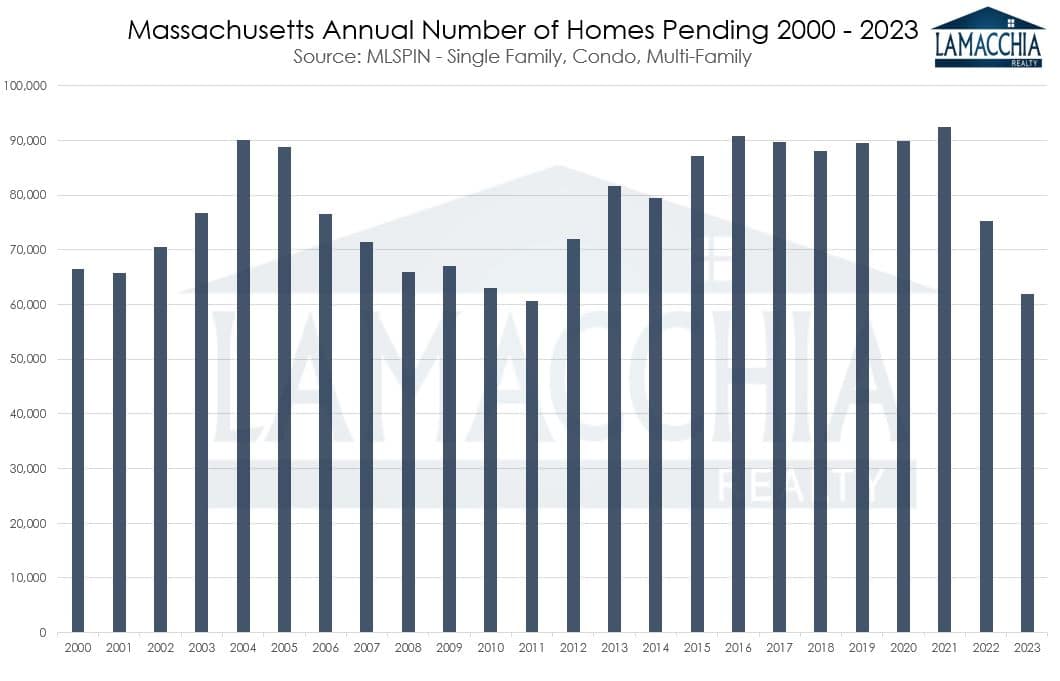

2022 was down in sales from 2021 just like this past year, and at that time, many were concerned that it was a sign the market was about to crash, something Anthony has repeatedly disproved. A year later, still no crash, which had more to do with the decrease in inventory than the decrease in sales. Sales being down in 2022 wasn’t much of a surprise, more of a relief, because the frenzied 2021 market was unsustainable and real estate was begging for a sense of normalcy. Slower market activity this year, however, is representative of the journey back to equilibrium. Regardless of how necessary a market adjustment is, it can be painful and 2023 didn’t disappoint.

This report breaks down sales, average prices, the number of active listings, and how many listings went under contract for 2023 compared to 2022 and discusses what is predicted to unfold in 2024.